Learn

- Share:

-

-

-

-

Optimizing Wealth Management with Grantor Retained Annuity Trusts (GRATs)

By Amy Piedmont, J.D., LLM, Vice President, Sr. Trust Relationship Manager and

Katherine “Kate” Gambill, J.D., Vice President, Sr. Trust Relationship Manager

Are you a high-net-worth individual with assets that are projected to appreciate or produce income? If so, a Grantor Retained Annuity Trust (GRAT) could be a game-changing strategy for your estate and tax planning.

In our series, “The Personal Trust Corner: A J.D.’s Perspective,” we aim to spotlight one planning strategy each month in response to the ever-changing Estate Tax Laws. These strategies can be employed individually or in combination.

For high-net-worth couples and individuals, estate planning often involves intricate strategies designed to safeguard wealth and ensure a solid financial legacy. With the Federal estate tax generally at 40% on an individual’s entire estate, we understand that this issue is top of mind for most individuals. This month, we turn the spotlight on GRAT.

Understanding GRATs

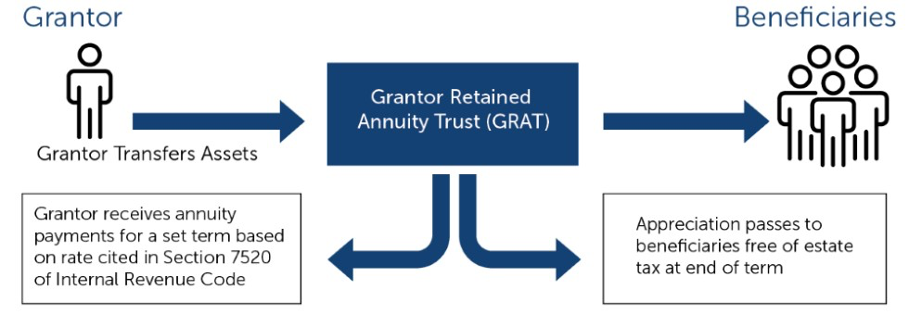

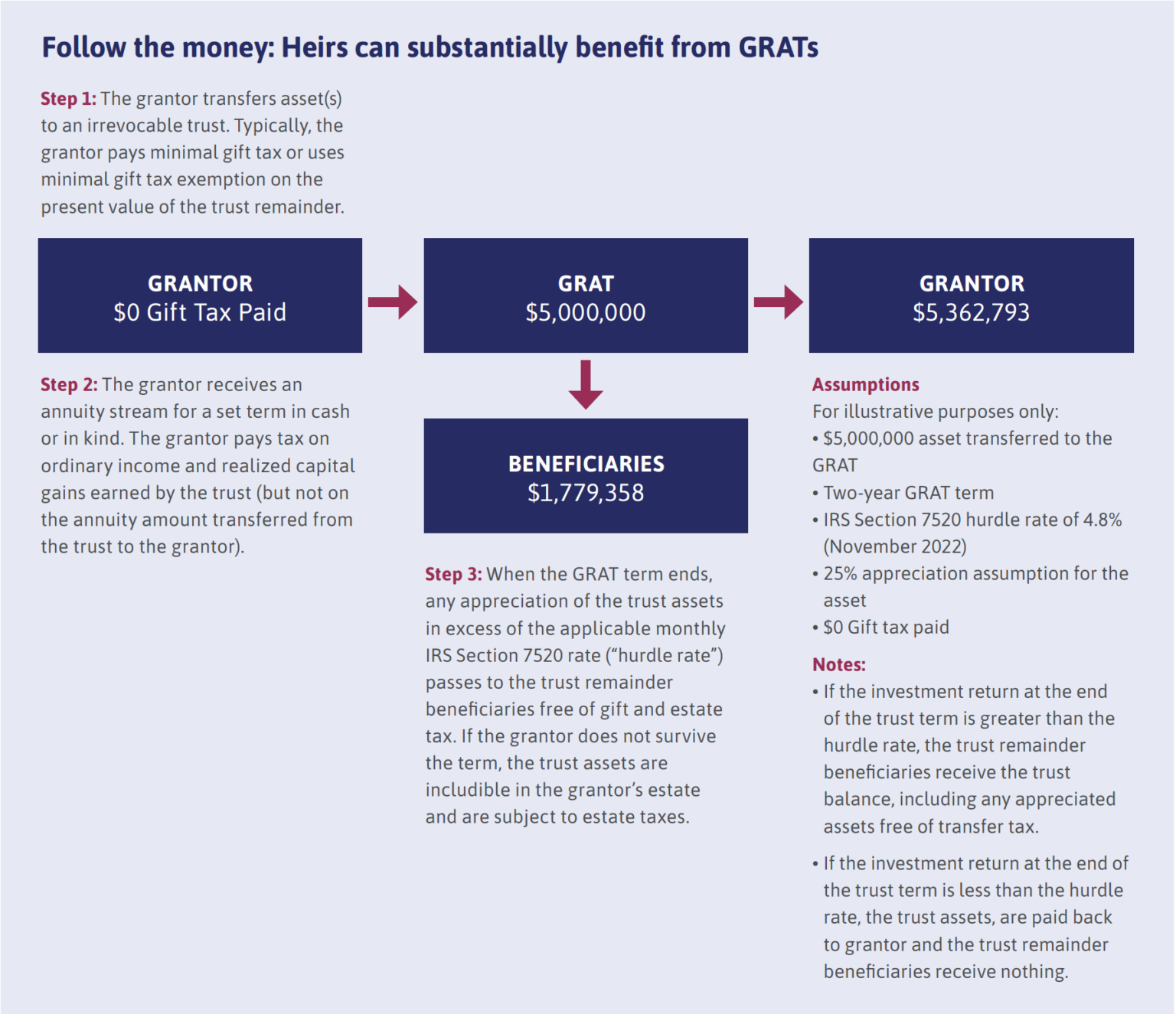

A GRAT is a type of trust that allows you, the grantor, to transfer assets to beneficiaries while receiving a stream of annuity payments for a set term.

Essentially, a GRAT allows you to "freeze" the value of an asset, excluding future appreciation or income from your taxable estate. Plus, you can continue to pay income tax for the trust without the payment being considered a taxable gift, further reducing your estate tax liability. The annuity payments you receive are calculated based on the fair market value of the assets at the time they are transferred into the trust.

How GRATs Calculate Asset Appreciation

The appreciation of assets is calculated based on their projected growth, including income, from the date of transfer to the trust until the grantor’s death. This appreciation can be calculated using an investments growth rate, residential real estate value growth rate, or the Consumer Price Index rate. These rates can be manually adjusted to align with your specific financial situation.

Splitting Gifts Between Spouses

In instances where there is a less wealthy spouse who may forgo taking advantage of their annual gift exemption, splitting the gift is a great option (so long as the spouse will not benefit from the gift). Spouses can effectively “split” gift by filing a gift tax return and making the proper election. This means the gift is considered to have been made 50/50 by each spouse, doubling the Annual Exemption Amount and potentially reducing the taxable estate.

Crummey Powers

Crummey Powers allow a gift to the trust to be considered a gift of present interest, thereby qualifying for the annual gift exemption. A Crummey Letter will advise the beneficiary of their right to withdraw, but only for a short period of time after the contribution, ideally allowing the assets to grow.

Grantor Trust Status, for federal income tax purposes, is where a grantor retains certain rights over irrevocable trust property such as the ability to “swap” assets of equal value. The IRS will consider the grantor the owner of the assets for purposes of income, deductions and credits, but not for federal estate tax purposes, thus reducing the grantor’s taxable estate.

Your attorney may discuss an Installment Sale to a Grantor Trust to ensure cash flow never becomes an issue. This occurs when a grantor sells assets to an irrevocable trust with Grantor Trust Status (disregarded for income tax), and in exchange receives a promissory note (note must bear interest at Applicable Federal Rate).

Toggling Off Grantor Trust Status is a great option to consider if there is ever any concern that your GRAT will potentially be larger than your estate. This gives you the option to eventually change your Grantor Trust to trust without Grantor Status, meaning the trust income, deductions and credits are taxed to the trust, not the grantor.

In conclusion, a GRAT can be a powerful tool for wealth management, particularly for high-net-worth individuals.

By understanding and leveraging the mechanisms of a GRAT, you can optimize the transfer of your wealth to the next generation while minimizing your estate tax liability. However, like all financial strategies, it also comes with its own set of risks and considerations. At Personal Trust, our commitment is to guide you through this intricate landscape.

Please reach out to our Senior Trust Relationship Managers: Amy Piedmont, J.D., LLM, Vice President, in Pensacola, Florida and Katherine Gambill, J.D., Vice President, in Atlanta with any questions or to start a conversation regarding estate planning. We welcome the opportunity to introduce you to how Synovus Trust Company can serve your needs.

Important disclosure information

Asset allocation and diversifications do not ensure against loss. This content is general in nature and does not constitute legal, tax, accounting, financial or investment advice. You are encouraged to consult with competent legal, tax, accounting, financial or investment professionals based on your specific circumstances. We do not make any warranties as to accuracy or completeness of this information, do not endorse any third-party companies, products, or services described here, and take no liability for your use of this information.