Learn

- Share:

-

-

-

-

Investing For Chickens: A Deep Dive on Buffered ETFs

By Chris Brown, CIMA®, CRPC™

Vice President — Investments

When Fear Strikes

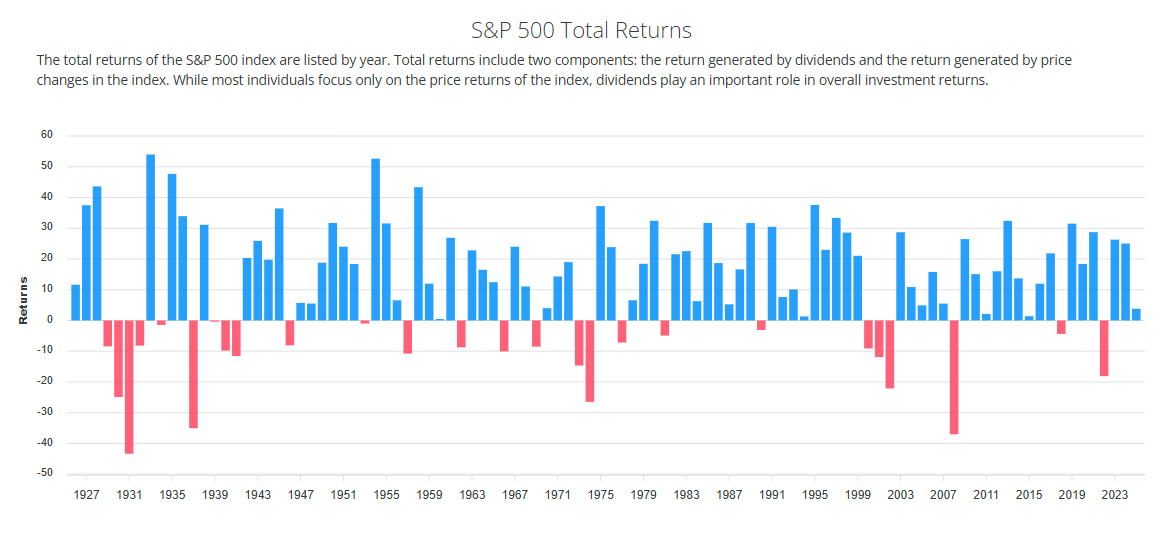

Investing in the equity markets can be extremely rewarding for long-term investors. Studies have shown that long-term diversified equity investing has been one of the top solutions to hedge against inflation, along with commodities like gold and real estate investments. Investing in a high-quality diversified equity portfolio has become easier and easier over the past decade. Staying invested during volatile market conditions is the biggest challenge for your investment outcomes. I’ve listened to long-term investors during good-to-flat market conditions — with a sound and active financial plan — tell me, “I’m comfortable investing over the long term,” or “as long as I’m diversified, my investment will be fine,” or “if I see the stock market go down, I’ll just buy the dip!”

In reality, when the bear market comes out of hibernation, irrational fear begins to take over the rational investment decisions and financial planning that you have created over the past few years. And before you know it, you’ve exited the markets and have blown up your plan. Mike Tyson once said it best, “Everyone has a plan until you get punched in the face.”

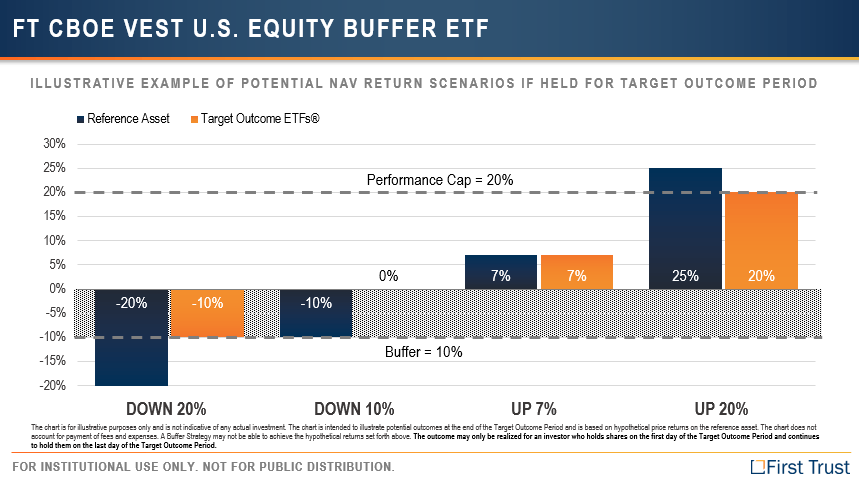

But what if there was a way to invest and not absorb the large down swings of the stock market? What if you could receive 50% to 70% of the upside returns and avoid 70% to 100% of the downside volatility. It almost sounds too good to be true. Not quite. Buffered ETFs, or Defined-Outcome ETFs, provide these forementioned features, but they are all not created equal.1

S&P 500 Returns Year-over-Year

How They Work

The investment company that provides the Buffered ETF buys an index, like the S&P 500 (most commonly used), and incorporates the use of option contracts to limit the downside volatility. For instance, I buy SPY (the S&P 500 ETF) and then purchase rolling monthly put option contracts to pay my account if equity markets fall to the options strike price. If the market keeps moving up, then your SPY position continues to increase in value and provides continued growth performance up to a certain cap each year. In short, you are investing your funds to receiving market participation with a capped upside return and a decreased downside market exposure for a defined period. Many buffered ETF investments have various downside protection amounts over an annual investment period. The downside buffer may protect up to 10%, 15%, 20%, and some provide up to 100% market volatility protection. A higher downside protection feature usually results in a more limited participation of upside returns based on the indexed investment.

Why So Popular now?

According to Suzanne McGee with Thomson Reuters, “Over the last three years, assets invested in these products have soared to $41 billion or more from less than $10 billion.”2

One of the largest, wealthiest and most experienced U.S. investor, collectively, is the baby boomer generation. They are currently between the ages of 60 and 78-years-old and comprise 22% of the U.S. population. The boomer generation had taken charge of their own investments and have amassed more than $10 trillion in mutual fund and equity assets over the past 50 years. This is due to increased personal savings in corporate retirement accounts, as traditional pensions have decreased dramatically for private sector employers over the past 30 years. Now, with a shortened investment time horizon, many baby boomer investors like the idea of equity-like returns but may not have the time to make up market downturns, especially while taking income distributions from their accounts.

For younger investors, GenX, Millennials and older Gen Z adults, who have now entered the workforce, are living in an instant information and technology-driven economy. Investors can receive information overload that creates behaviors that may include the following common mistakes:

- Market timing — moving cash in and out of the markets to avoid large downturns; the S&P 500 provided 20% higher returns in 2023 and 2024, so the thinking becomes, “We are due for a big downturn!”

- Paralysis by analysis — investors study market conditions and watch every informational videos to gauge when and how much they can invest, which may delay when they start investing in the markets.

- The Burned investor — Those who had a bad market experience in the past and just moved cash to money markets and CDs.

Buffered ETFs may assist in providing more certainty for defined investment outcomes for the risk averse investor who may keep one hand hovering over the sell button.

Tax Efficiency

Buffered ETFs can also offer some tax efficiencies. Many ETFs allow for a tax-deferred savings, as the strategy may earn unrealized capital gains. And buffered ETFs held for more than 12 months, when sold, are usually taxed as long-term capital gains. If you do not have current income needs from your investments, you can avoid the interest income that is often associated with the fixed income investments like bonds or annuities, which create taxable income based on your earned income tax bracket. When planning for investors who are 65 and older, earned income produced by fixed income investment strategies may push your modified adjusted gross income (MAGI) above the annual limits ($106,000 for individuals; $212,000 for joint filers in 2025), which may increase your Medicare Part B and Part D premiums.

Understanding the features and benefits of a Buffered ETF allocation as a part of your financial plan is paramount. Creating a financial plan that addresses your investment objectives, risk tolerance and investment time horizon will help you determine whether your plan needs growth, income, downside volatility protection, or all of the above. The most successful investment plan will be the allocation mix that allows you to ride out the stormy seas of volatile market conditions.

Important disclosure information

Asset allocation and diversifications do not ensure against loss. This content is general in nature and does not constitute legal, tax, accounting, financial or investment advice. You are encouraged to consult with competent legal, tax, accounting, financial or investment professionals based on your specific circumstances. We do not make any warranties as to accuracy or completeness of this information, do not endorse any third-party companies, products, or services described here, and take no liability for your use of this information.